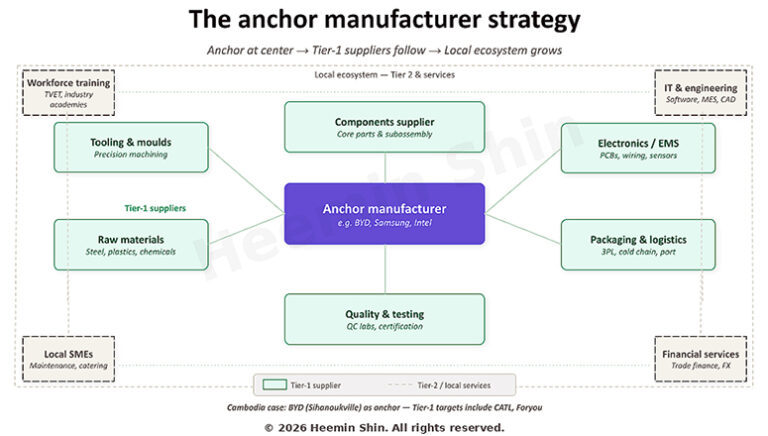

The manufacturing anchor strategy

Workers at a garment factory in Phnom Penh. Cambodia added 310 new garment factories in 2025, bringing the total to 1,876 factories. KT/Pann Rachana

Workers at a garment factory in Phnom Penh. Cambodia added 310 new garment factories in 2025, bringing the total to 1,876 factories. KT/Pann Rachana

#Opinion

Cambodia does not need more investment approvals. It needs one manufacturer that changes everything around it

Columns 1 through 4 diagnosed the problem. This column begins Part III: where Cambodia can win. The first answer is manufacturing.

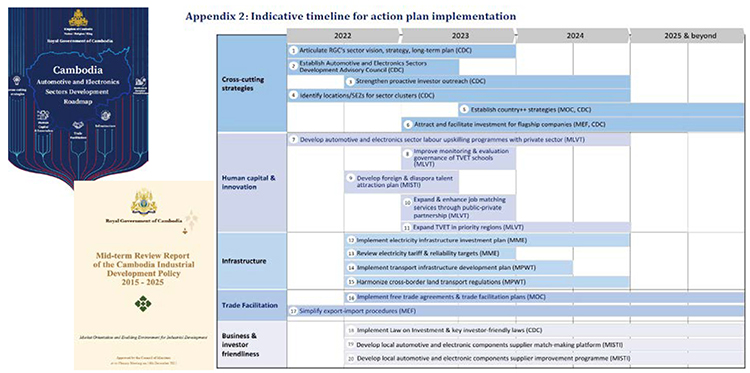

Cambodia does not lack good plans. Two reports on CDC’s public website, the Industrial Development Policy Mid-Term Review (2021) and the Automotive and Electronics Sectors Development Roadmap (2022) (hereafter “2022 Roadmap”), identify the right targets, the right bottlenecks, and the right solutions. Initiative 6 of the 2022 Roadmap calls for attracting flagship companies.

Three years later, the only meaningful anchor to arrive is BYD, producing 10,000 vehicles per year in Sihanoukville. The problem is not analysis. The problem is execution.

Table 1. Cambodia Automotive and Electronics Sectors Development Roadmap & Mid-term Review Report

Source: (lefthand): available at cdc.gov.kh

Source (righthand table): Cambodia Automotive and Electronics Sectors Development Roadmap, CDC/BCG. (Initiative 6 of the 2022 Roadmap: Attract and facilitate investment for flagship companies. Scheduled to begin in 2023.)

A manufacturing anchor creates conditions for an ecosystem. It pulls Tier-1 and Tier-2 suppliers into the same geography. It sets quality standards that local suppliers must meet. It signals to every other company in its sector that Cambodia is a credible location. Without the anchor, small companies arrive in isolation. With it, they arrive as part of a system. Cambodia’s strategy must be anchor first, ecosystem second. The sequence is not optional.

Figure 1. The anchor manufacturer strategy

Note: TVET = Technical and Vocational Education and Training; MES = Manufacturing Execution System; QC = Quality Control.

The right dectors

Three sectors meet the core criteria today: actively relocating from China or Vietnam, Cambodia has a structural advantage, and the anchor pulls a supply chain behind it.

Electric vehicle parts assembly. BYD’s Sihanoukville plant is a signal, not a solution. Denso, Yazaki, Sumitomo, and Kyungshin are already making wiring harnesses in Cambodia for Thai and Vietnamese assembly plants, exactly the Country +1 model the 2022 Roadmap was built around. The next step is moving these companies into higher-value EV components: battery casings, converters, vehicle control units. And BYD’s Tier-1 suppliers, including CATL, Foryou, and Minth, are still sourcing from China. Cambodia needs to go to them now with a clear message: your anchor client is here, and following it is easier than shipping from Shenzhen.

Electronics sub-assembly. Minebea, SVI, and Sumitronics are already producing cables and connectors in Cambodia. A 2024 AMEICC study confirmed electronics and automotive components as priority sectors. The task is twofold: help existing players move into higher-value PCB assembly, and bring in larger EMS anchors that create a cluster. Malaysia’s trajectory shows what is possible.

Penang started with Intel and Motorola in the 1970s and today holds 13 percent of the global semiconductor test and packaging market.

Halal food processing. Halal Park Cambodia launched in September 2024. Cambodia participated in Malaysia’s MIHAS as a structured delegation in 2025. The global halal food market is $2.5 trillion and growing at over 9 percent annually. Battambang’s agricultural base provides raw material. The processing cluster does not yet exist. That is the opportunity.

How to attract them

Vietnam won Samsung not by having better tax rates. It won because the Prime Minister met the chairman directly, presented a confirmed site, guaranteed power, legally binding tax terms, and a direct government counterpart. Cambodia’s current sequence — company applies, CDC processes, company finds land, company deals with unstable power — produces garment factories. It does not produce anchors. Four things must change.

First, go to the companies. A dedicated PM-office unit, not CDC and not the Ministry of Commerce, should have a list of 20 to 30 target companies, a named contact at each, and quarterly outreach. Singapore’s EDB hired former corporate executives with authority to negotiate on the spot. Cambodia needs the same profile: people who speak the language of CFOs, not permit queues.

Second, bring the value chain, not just the anchor. 2022 Roadmap flagged this risk: local content in two-wheeler assembly is only 25 percent despite Honda and Suzuki operating here for years.

The anchor package must automatically extend incentives to co-locating Tier-1 and Tier-2 suppliers under a single umbrella registration, with binding local employment and technology transfer obligations.

Third, training must be part of the offer. Malaysia’s Penang PSDC is the model: Intel, HP, and Motorola co-founded a skills center with the state government in 1989, with government providing land and companies providing equipment and trainers. 2022 Roadmap proposed exactly this structure. Cambodia should make it standard in any anchor negotiation.

Fourth, designate two SEZs and stop approving new ones. 2022 Roadmap identified the absence of a cluster strategy as a primary challenge: automotive and electronics plants are dispersed across Cambodia in various locations, missing the network effects that concentration creates. Sihanoukville for EV and manufacturing; a Phnom Penh corridor for electronics. Invest everything into making those two world-class. One fully equipped SEZ beats twenty empty ones. On power: stable and affordable electricity is the prerequisite for any anchor commitment. How Cambodia solves that problem is the subject of Part 11.

Small companies will follow the anchor. They always do. But they follow an anchor, not a vacancy.

Next in this series (Part 6): ‘The Mekong Dollar’ — Cambodia is the only dollarized economy in mainland Southeast Asia. Every neighbouring country restricts capital outflows. Cambodia does not.

That structural difference, combined with a reformed capital market, could make Phnom Penh the dollar gateway for Mekong capital — a place where entrepreneurs list, investors exit, and regional money moves through a legal, transparent channel for the first time.

Author bio: Heemin Shin is a founding partner of Plateaux Capital, a private equity house based in New York, with prior roles as CFO of a Cambodian microfinance institution, managing director at Siguler Guff Company & LP, and founder of a fintech company he took to a successful exit. He writes in a personal capacity. Email: david@plateauxnewyork.com

-Khmer Times-